When I got my first job in Kampala, I thought I had finally made it in life. After years of lectures, coursework, internships, and endless applications, I was finally earning a “real salary.” The offer letter said I would earn UGX 1,500,000 per month, and honestly, my mind had already started spending the money before I even received it.

I imagined buying a better phone, helping my parents, upgrading my wardrobe, and maybe even moving into a slightly nicer apartment. To me, UGX 1.5 million sounded like wealth.

Then payday arrived.

I opened my mobile banking app with excitement, expecting to see the full amount. Instead, I saw a number much smaller than I expected. For a moment, I thought the company had underpaid me.

I rushed to check my payslip.

That was the day I learned the painful difference between gross salary and take-home pay.

A senior colleague noticed my confusion and laughed gently.

“Welcome to adulthood,” he said. “The government eats before you do.”

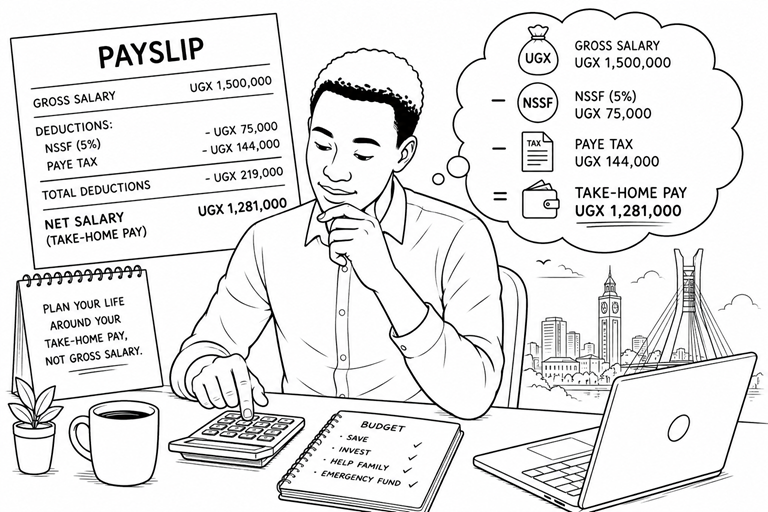

He explained that the salary written in the contract was my gross salary—the amount before deductions. What actually reaches your account is your net salary, also called take-home pay.

The biggest deduction for most employees in Uganda is PAYE (Pay As You Earn), which is income tax deducted by the employer before salary is paid. Depending on how much you earn, the percentage increases gradually. Then there is NSSF, where employees contribute part of their salary toward social security savings.

That afternoon, my colleague sat beside me and showed me how to estimate take-home pay properly.

He explained it in the simplest way possible.

First, start with your gross salary. Then subtract NSSF contributions. In Uganda, employees usually contribute 5% of their gross salary to NSSF.

For example, if your gross salary is UGX 1,500,000:

NSSF deduction would be:

5% × 1,500,000 = UGX 75,000

That leaves:

1,500,000 − 75,000 = UGX 1,425,000

Then PAYE tax is calculated based on the taxable income brackets set by the government. The higher your salary, the more tax you pay.

My colleague warned me about something many fresh graduates misunderstand.

“Never plan your life around gross salary,” he said. “Always plan around take-home pay.”

That sentence changed how I looked at money completely.

Many fresh graduates get excited when they hear big salary figures during interviews, only to feel disappointed after receiving their first payslip. But the problem is not always low pay—it’s usually lack of understanding about deductions.

He also taught me another important lesson: payslips matter.

Most young employees ignore them completely. They only check whether money entered the account. But a payslip helps you understand your deductions, taxes, loans, allowances, and savings contributions. It also helps when applying for visas, loans, rentals, or future jobs.

As months passed, I became more financially aware. Before accepting any job offer, I stopped asking only, “How much is the salary?” Instead, I started asking, “What will my approximate take-home pay be after deductions?”

That small change saved me from unrealistic expectations.

I also learned that earning more money does not always mean keeping much more money. Sometimes a salary increase pushes you into a higher tax bracket, meaning deductions increase too. Understanding this helps employees make smarter financial decisions instead of emotional ones.

For fresh graduates entering the workforce, one of the smartest habits you can develop is financial awareness. Learn how taxes work. Understand your payslip. Budget using net salary, not gross salary. Save early, even when the amount feels small.

Because the truth is, your first salary is not just income.

It is your first lesson in financial responsibility.